Eliminating tax subsidies that primarily benefit the plutocrats is urgently needed if we are to preserve the middle class and our economy.

Martin Lobel, JD specializes in crisis management and represents many investigative reporters in addition to being an expert on the constitutionality of state taxes. He has written extensively on tax issues.

***

In Part 1 of this two-part series, Martin Lobel detailed how the Tax Cuts and Jobs Act (TCJA) gave massive tax cuts to the very rich, massively increased budget deficits, increased incentives to move jobs and profits offshore — and minimally increased investment in productivity. All of these events could trigger a revolt. As Lobel put it,

If you build a dam without a spillway, eventually the water pressure will break the dam, sweeping away everything below it. On the other hand, if you build a dam with a spillway, you can channel the pent-up power in useful ways to everyone’s benefit. Enacting the TCJA was like building a dam in the dark to benefit a very small sector of the economy — and to the detriment of almost everyone else. Once the rest of the population realizes what’s happened to them, they would be justified in taking action to defend their own interests. The danger is that any action taken without thinking through the long-term consequences may only make things worse.

***

Preventing a Revolt

Expose the Role of Money in Lawmaking: Money talks, and you can see in the TCJA the impact of hidden money and well connected lobbyists. The bill was largely drafted in secret. The rich got a lot richer. Sheldon Adelson, for example, who recently gave $30 million to the Republican House PAC and $25 million to the Republican Senate PAC, received about a $700 million tax cut from the TCJA.2

The Koch brothers, according to press reports, gave $20 million to support passage of the TCJA and received tax benefits worth between $1 billion and $1.4 billion.3 As the late Senator William Proxmire (D-WI) used to say, “The more complex the tax provision, the more likely it is an unjustifiable subsidy.” Clearly, we need to make all campaign contributions public as soon as they are made. No longer should we allow political money to hide behind PACs or super PACs or 501(c)(4) organizations. All political spending by corporations should be publicly disclosed and subject to the approval of the company’s board of directors.

Role of the Media: The media must do a much better job of exploring and explaining economic issues so that the public understands what lies behind the political catch phrases that are so misleading. This means the end of the he-said-she-said reporting that passes for analysis today. It means that reporters will have to dig deeper and read analyses from the Congressional Research Service,4 Tax Notes, the Tax Policy Center, the Institute on Taxation and Economic Policy, the Center on Budget and Policy Priorities, Taxpayers for Common Sense, the Tax Foundation, the American Enterprise Institute, and others.

For example, there have been lots of stories about how the estate tax, aka the “death tax,” has cost farmers their farms and justified the $11.2 million estate tax exemption for couples — but little about the economic research report from the US Department of Agriculture that could not find one farmer who lost his farm because of the estate tax.5

Traditional Goals of Tax Reform: Greater Equity, Efficiency, Simplicity.

Eliminating different rates for different forms of organizations would also simplify the tax code. Requiring different types of corporations, LLCs, LLPs, master limited partnerships, pass-throughs, etc. to pay the same rate of income would eliminate much unnecessary complexity and compliance costs. Indeed, it might be easier to eliminate all taxes on such entities, but require them to treat investors as employees. The entity would pay the investor their proportionate share of the profit less, say, 30 percent, which it would pay to the IRS. It would then issue W-2s to the investors showing that the entity paid 30 percent of the profit to the IRS, which the investors could use as a non-transferable tax credit against the taxes they owed. That would significantly lower administrative costs of collecting the income and would diminish the incentive for investors to hide income offshore.8

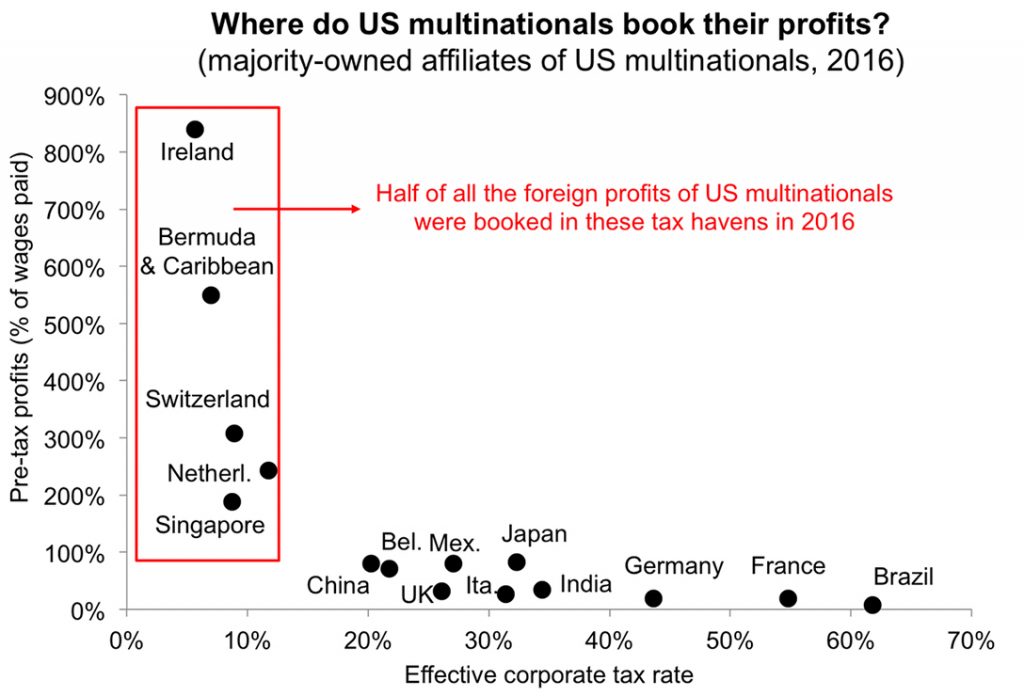

Eliminating Transfer Pricing and going to a Unitary Accounting system for multinational corporations to better account for where the income is really earned. Companies would no longer be able to hide their profits in low-tax countries, minimizing their tax obligations in the US. The amount of multinational profit-shifting is so significant that it distorts macroeconomic statistics.9 For example, in 2017, American-based multinational companies reported 43 percent of their foreign earnings in five small tax havens: Bermuda, Ireland, Luxembourg, Netherlands, and Switzerland. Yet, these countries accounted for only 4 percent of the companies’ foreign workforce and 7 percent of their foreign investments.10

The TCJA exacerbated the problem by exempting income from taxation that the companies claim they earned offshore. It adopted a complex form of territorial taxation, encouraging the race to the bottom as the multinationals manipulate various countries to lower tax rates to attract them.11 But, as every IRS commissioner who has testified on the topic has admitted, the IRS lacks the resources to police the efforts to hide profits.

The benefits of eliminating deferral of overseas income and adopting a unitary accounting system are overwhelming, which is why the multinationals fought so hard for the territorial system.12

Using refundable tax credits instead of deductions to encourage certain activities and treat every income group, especially the lower-income groups more fairly.13

Imposing Inheritance Taxes Instead of Estate Taxes. Because of the high exemption from paying estate taxes, significant amounts of wealth are transferred tax-free, leading to even more concentration of wealth. Shifting to an inheritance tax with, for example, a $2 million exemption would allow the recipients to be taxed at their individual rate on the increase in value between the time it was acquired and the time it was transferred to the beneficiary.14

Providing Adequate Funding for the Internal Revenue Service so that it can fairly enforce the tax code and help cut the deficit.15 Right now it has to figure out what Congress intended in the TCJA without any real public hearings and without adequate resources to effectively collect the revenue it should.16

There are lots more reforms that have been discussed in Tax Notes and elsewhere, like a small tax on the sale of securities to curb speculation, but the question is whether and when we will be forced to implement them to prevent more radical proposals by politicians who want to capture public outrage. Capitalism has allowed us to grow and prosper, but it also needs a policeman.17

Democracy provides a means of policing the concentration and abuse of wealth, but we know that it takes a crisis to energize government to act. Will it be a recession or worse? A trade war? A political crisis? We don’t know, but we do know that we had better be prepared with some well-thought-out reforms to meet the public’s demands for a more equal distribution of wealth and more rapid growth in income.

Related front page panorama photo credit: Adapted by WhoWhatWhy from sign Adam Fagen / Flickr (CC BY-NC-SA 2.0), IRS building Tim Evanson / Flickr (CC BY-SA 2.0), and sky Vincent Parsons / Flickr (CC BY-NC 2.0).

Endnotes

- For a partial listing, see, “The Games They Will Play: Tax Games, Roadblocks, and Glitches Under the New Legislation.”

- “Trump Tax Cut Unlocks Millions for a Republican Election Blitz“; “Sheldon and Miriam Adelson Give $25M to Help Republicans Keep Their Majority in the Senate.”

- “Koch Brothers Could Get Up to $1.4 Billion Tax Cut From Law They Helped Pass.”

- Indeed, most of the myths underlying the TCJA were dispelled in a Congressional Research Service report titled “Corporate Tax Reform: Issues for Congress” by Jane G. Gravelle dated Sept. 22, 2017, Tax Notes Doc. 2017-72370. Unfortunately, Congress chose to listen to the lobbyists.

- https://www.ers.usda.gov/topics/farm-economy/federal-tax-issues/federal-estate-taxes/.

- See Piketty, Capital in the Twenty-First Century (2014).

- See Ganesh Sitaraman, The Crisis of the Middle-Class Constitution (2017).

- Martin Lobel, “Eliminate the Corporate Income Tax and Level the Playing Field,” Tax Notes, Dec. 2, 2013, p. 967; Eric Toder and Alan D. Viard, “Major Surgery Needed: A Call for Structural Reform of the U.S. Corporate Income Tax” (2014), but see Reuven S. Avi-Yonah, “Is Corporate Integration a Good Idea,” Tax Notes, June 20, 2016, p. 1697; Edward D Kleinbard, “The Trojan Horse of Corporate Integration,” Tax Notes, Aug. 15, 2016, p. 957.

- Bruner, Rassier, Ruhl, NBER working paper No. 24915. If multinationals had to use unitary accounting it would have increased US GDP by $3.5 trillion between 1994 and 2014.

- “Offshore Shellgames 2017“; see also, “Who Owns the Wealth in Tax Havens? Macro Evidence and Implications for Global Inequality,” Alstad Seater, Johannesen, Zucman, which found that about 10 percent of global wealth is held in tax havens.

- Daniel N. Shaviro, “The New Non-Territorial U.S. International Tax System, Part 2,” Tax Notes, July 9, 2018, 171.

- See, e.g., Martin Lobel, “Worldwide Apportionment Would Stop Export of Jobs and Profits,” Tax Notes, June 18, 2012, p. 1539.; Martin Lobel, “Territorial Taxation: An Invitation to Tax Avoidance and Evasion,” Tax Notes, January 5, 2009, p. 109. Reprinted in Tax Notes International, Feb. 9, 2009, p. 519; Kimberly A. Clausing and Reuven S. Avi-Yonah, “Reforming Corporate Taxation in a Global Economy: A Proposal to Adopt Formulary Apportionment,” The Hamilton Project, 2007; Reuven S. Avi-Yonah, “Guilty as Charged: Reflections on TRA 17,” Tax Notes, Nov. 20, 2017, p. 1131; Kimberly Clausing, “Testimony before the Senate Finance Committee,” Oct. 3, 2017, Tax Notes Doc.2017-71962; Stephen E. Shay, “Directions for International Tax Reform,” Oct. 3, 2017, Tax Notes Doc 2017-71962; Fleming, Peroni and Shay, “Incorporating a Minimum Tax in a Territorial System,” Tax Notes, Oct. 2, 2017, p. 73. Bill Parks, “Why Objections to Sales Factor Apportionment Are Bogus,” Tax Notes, Nov. 20, 2017, p. 1155; Jeff Ferry, “Revenue Gains From Sales Factor Apportionment Corp Income Tax,” Tax Notes, Nov. 27, 2017, p. 1313; Eric Toder, “Territorial Taxation: Choosing Among Imperfect Options,” Dec. 2017.

- Lily L. Batchelder, Fred T. Goldberg, Jr. And Peter T. Orszak, “Efficiency and Tax Incentives: The Case for Refundable Tax Credits,” 59 Stan. L. Rev. 23 (2006).

- Lily L. Batchelder, “Taxing Privilege More Effectively: Replacing the Estate Tax with an Inheritance Tax,” The Hamilton Project, June 2007.

- According to the IRS there are 616 companies with $20 billion or more of assets. As recently as FY 2010 96 percent of them were audited, but in FY only 54 percent were audited. The magnitude of the revenue loss can be extrapolated from the 331 that were audited which uncovered $10.4 billion in unreported federal taxes. “Nearly Half of Corporate Giants Escape IRS Audit in 2017.”

- “Manafort, Cohen cases reveal weaknesses in enforcement of tax and election laws,” Washington Post, Aug. 26, 2018, p. A1; “Martin Lobel, The IRS is in Crisis and the Tax Community Needs to Help,” Tax Notes, Dec. 14, 2015, p. 1407; reprinted in Huffington Post, Dec. 15, 2015.

- There simply is no such thing as a market free of all political bias. The most important economic resource is trust in the future, and this resource is constantly threatened by thieves and charlatans. Markets by themselves offer no protection against fraud, theft and violence. It is the job of political systems to ensure trust by legislating sanctions against cheats and to establish and support police forces, courts and jails which will enforce the law. When kings fail to do their jobs and regulate the market properly, it leads to loss of trust, dwindling credit and economic depression.