TCJA gave massive tax cuts to the very rich, massively increased budget deficits, increased incentives to move jobs and profits offshore — and minimally increased investment in productivity.

Martin Lobel, JD specializes in crisis management and represents many investigative reporters in addition to being an expert on the constitutionality of state taxes. He has written extensively on tax issues.

***

We are in the early stages of a likely revolt against “the Establishment.”1 Small wonder. Because of government policies for the last 50 years, essentially the entire growth in GDP has gone to the top 1 percent. And primarily to the top 0.01 percent, aka the “plutocrats.”

As middle class voters understand how badly they have been treated economically, they’re likely to demand changes similar in scale to those of the 1890s or the 1930s2 — unless government policies are changed soon.

The consensus among political commentators is that one of the key factors in Donald Trump’s election is that he captured the resentment of a significant portion of the middle class who felt their economic and social concerns were being ignored by the Establishment3 — epitomized by Hillary Clinton, who was seen as spending too much time in the Washington bubble.

Many voters understood instinctively that the Establishment was far more concerned about the welfare of the plutocrats (including liberal plutocrats) who funded their campaigns than about the average middle class voter. As Anthony Downs pointed out in his book An Economic Theory of Democracy, rational politicians will do whatever is necessary to maximize the number of votes they get, which means they will vote the way their constituents want on the few issues that attract public attention — while voting to please their campaign contributors the rest of the time.

Trump’s Tax Cuts and Jobs Act (TCJA) may be the furthest swing of the pendulum toward the plutocrats, and may trigger a middle class voter backlash against the Establishment. But before we get to that, it’s worth examining the evidence supporting the assertion that government policies, most recently the TCJA, have shifted almost all of the GDP growth to the top 1 percent.

Income Shift to the Top 1%

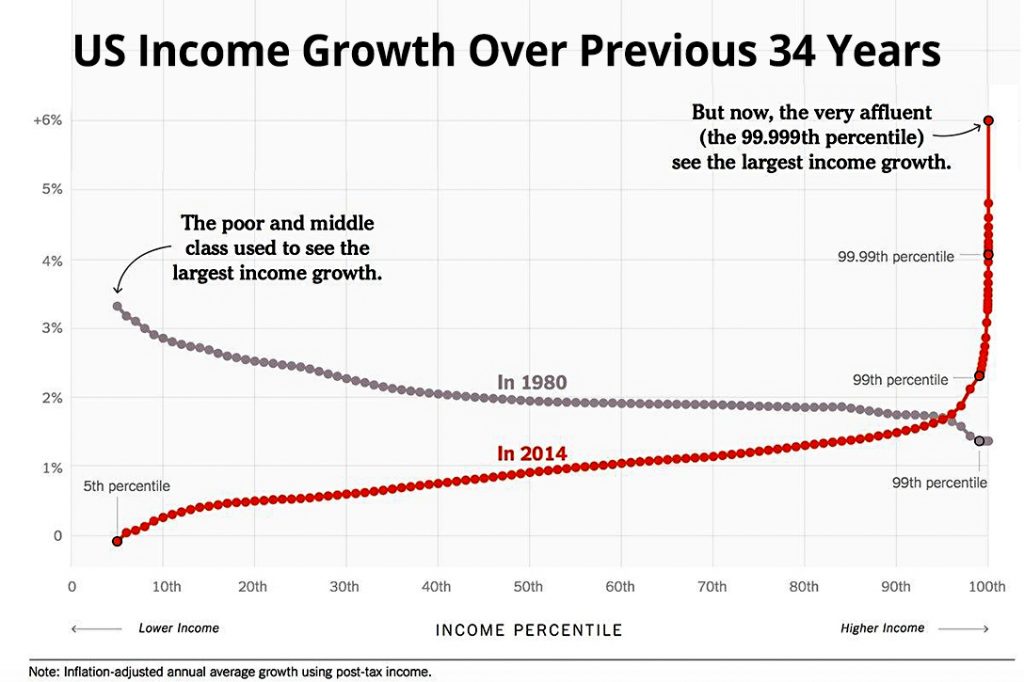

Writing in the May 2018 Quarterly Journal of Economics, one of the premier peer-reviewed economic publications, Thomas Piketty, Emmanuel Saez, and Gabriel Zucman found:

- Inequality surged between 1980 and 2014 as the income of the bottom half of the population stagnated while the income for the top 1 percent of the population increased by 205 percent and for the top 0.001 percent by 636 percent.

- Put another way, during the same period, the bottom half’s share of the national income collapsed from 20 percent to 12 percent, while the income share of the top 1 percent increased from about 12 percent to 20 percent. Or to put it yet another way, the top 1 percent’s share of the economy is almost twice as large as the bottom 50 percent’s share.

- The upsurge of top incomes between the 1970s and 1990s was mostly wage-driven, but for the last 15 years income at the top mostly comes from investments in stocks and bonds.

- The reduction in the gender gap has mitigated income inequality but it is still significant. As of 2014, women make up only 16 percent of the top 1 percent of wage earners and 11 percent of the top 0.1 percent.

For the graphically inclined, here’s a chart showing the dramatic shift in income:

Why the TCJA May Trigger the Revolt

If you build a dam without a spillway, eventually the water pressure will break the dam, sweeping away everything below it. On the other hand, if you build a dam with a spillway, you can channel the pent-up power in useful ways to everyone’s benefit.

Enacting TCJA was like building a dam in the dark to benefit a very small sector of the economy — and to the detriment of almost everyone else.

Once the rest of the population realizes what’s happened to them, they would be justified in taking action to defend their own interests. The danger is that any action taken without thinking through the long-term consequences may only make things worse.

For those who think “it can’t happen here,” consider what happened in Argentina because of politically motivated economic errors.4 In 1912, Argentina’s per capita GDP exceeded that of the United States. By 2017, having survived several bouts of runaway inflation and bankruptcy, Argentina’s per capita GDP was 82 percent of the world’s average,5 while the US’s was more than four times larger.6

The TCJA is based on false premises, and is incredibly complicated and riddled with errors because it was drafted without any public hearings7 and jammed through Congress on a party-line vote. Perhaps the bill was so badly drafted because the experts at Treasury were not involved.

In fact, the TCJA fails the three traditional goals of tax reform: greater equity, efficiency, and simplicity.8

Let’s examine the key underlying assumption: TCJA’s tax cuts will pay for themselves.

That’s a theological argument, unsupported by any evidence.9 In fact, it is contrary to all available evidence. For example, in 2012, Gov. Sam Brownback (R-KS) signed a bill that cut Kansas’s top tax rate, and exempted pass-through business income from taxation, promising that the bill would spur investment in Kansas and pay for itself. (A pass-through entity’s income is not taxed at the corporate level — it is only taxed at the individual owners’ level.)

The result was that real GDP growth in Kansas was about 75 percent of US GDP growth (6.1 percent versus 8.3 percent) and private employment growth was about 5 percent in Kansas versus 9.1 percent in the US overall.10

The number of pass-through businesses greatly exceeded expectations. The state expected 191,000 more businesses to take advantage of the tax break, far less than the increase of 330,000 pass-through businesses that actually occurred.

That shift significantly increased the tax revenue loss.11 The tax package reduced state revenue by nearly $700 million a year, a drop of about 8 percent from 2013 to 2016, forcing officials to shorten school years, delay highway repairs, and reduce aid to the poor.

The budget deficit and the flight of industry to other states with better education and infrastructure finally forced the legislature to repeal Brownback’s plan and impose a tax on pass-throughs.12 Brownback resigned as governor and became our “ambassador at large for international religious freedom” in January of 2018.

Despite the expressed belief by its sponsors that TCJA tax cuts would pay for themselves by increased economic activity, the evidence so far is that this is not so.

All that TCJA has accomplished is to provide massive tax cuts for the very rich, massive increased budget deficits, massive increased incentives to move jobs and profits offshore — and minimally increased investment in productivity, because the economy was already operating at or near full employment.

It’s worth examining each of these failures.

Massive Tax Cut for the Rich, But Not for Workers: According to the Tax Policy Center, by 2027 more than 53 percent of Americans would pay more in taxes while 82.9 percent of the TCJA’s benefit would go to the top 1 percent.13 Put another way, by the end of 2025 tax cuts since 2001 will grow to $10.6 trillion. Nearly $2 trillion of this amount will have gone to the richest 1 percent. By then, the total impact on the deficit will be $13.6 trillion, including interest payments.14 But it gets worse.

Corporate Tax Cuts Benefit the Rich, Not Productivity: According to proponents of the TCJA, cutting the corporate tax rate from 35 percent — which almost no companies actually paid — to 21 percent would increase investments in productivity, leading to increases in wages. But what actually happened?

As predicted by most economists, there was a significant increase in stock buybacks, which prop up stock prices,15 and in income for executives.16 In 2018 stock buybacks totaled over $1 trillion, most of which went to the very rich, who can convert ordinary income into capital gains by selling stock.17

Interestingly, those buybacks have really only maintained the price of the stocks.18 Very little of the tax cuts has gone into productive investments or paying down debt which, for about one-third of multinational companies, increased to $5 of debt for every $1 of earnings. As a result. these companies face a significantly increased risk of failure from an interest-rate increase, or a recession, or a trade war, according to Steven Pearlstein’s analysis in the Washington Post.19

In the meantime, average CEO compensation (including stock options) at the 350 largest firms increased in 2017 to $18.9 million, a 17.6 percent increase over 2016. At the same time, the average worker’s compensation increased by only 0.3 percent, a compensation ratio of 312 to 1. CEO compensation rose much faster than stock prices or corporate profits between 1978 and 2017 — and many times faster than the growth in the typical worker’s compensation.20

For the average worker, wage gains (2.7 percent) have been exceeded by inflation (2.9 percent) since the beginning of 2018,21 despite the historically low unemployment rate of 3.9 percent.22 But what about the benefits the workers were supposed to get from the TCJA?

The drop in effective tax rates due to TCJA is more dramatic for high-income households. For example, in 2018, TCJA reduced the typical total effective tax rate by 5.5 percent for the poorest fifth of Americans and by 5.7 percent for the middle fifth of Americans. The reductions in effective rates were far more impressive for the richest households — 7.4 percent for the richest 1 percent and 8.4 percent for the next richest 4 percent.23

TCJA Increased the Deficit Dramatically: Although politicians like to hand out tax cuts or subsidies because of their immediate impact, they are rarely concerned with the long-term consequences — since it’s the children or grandchildren of their constituents who will have to pay for them, long after the politicians have left office.

There is little evidence that TCJA’s tax cuts have improved the economy, since it was already operating at full employment levels.24 Unfortunately, the approximately $1.4 trillion increase in the deficit caused by the tax cuts and increased spending by Congress will be felt primarily by the middle class.

After TCJA narrowly passed Congress, Republican leadership “discovered” the deficit it created and trotted out their old proposals to solve the deficit by cutting social spending like Medicare and Social Security,25 thereby increasing the burden on the middle class.26 The deficit increased by 21 percent in the first 10 months of 2018 fiscal year.27

Both the Office of Management and Budget (OMB) and the Congressional Budget Office (CBO) have predicted dire results for the economy from the budget deficit.

OMB has projected a 2018 budget deficit of $779 billion.28 And, the CBO projects the deficit will raise from 78 percent of GDP in 2018 to 118 percent in 2038.29 In order to reduce the ratio of debt to GDP to the current 78 percent in 15 years, Congress would have to raise taxes and/or cut spending by $340 billion, or about $1,000 per person, in 2019, and continue to do so for each succeeding year.30 Economists are also concerned that by increasing the deficit we are limiting our ability to fight recessions — or worse — in the future.

TCJA’s Impact on Job Creation: This is likely to be principally among accountants and lawyers who struggle to interpret its complex provisions.31 Congress decided to lower the tax rate for pass-through income, which it didn’t really define coherently, by allowing sole proprietors and owners of some pass-through businesses to deduct 20 percent of business-related income so that only 80% of their income was taxable.

Lawyers and doctors can’t get the tax reduction on pass-through income but real estate developers can. Why? Because the law says so. Is there a rational justification for such a decision? None that is apparent, but the IRS’s proposed regulations for Section 199A — the pass-through income provision in the TCJA — do give an idea of the complexity and cost of implementing such a provision.

The proposed regulations are 184 pages long and estimate the compliance cost to businesses will be about $1.3 billion.32 A quick review of articles in Tax Notes shows how many questions remain about the applicability of pass-throughs to various businesses. But those with incomes of $500,000 to $1 million or more will be the principal beneficiaries.33

A little knowledge of what happened in Kansas when pass-throughs were not taxed should have alerted Congress to the many problems they created. But, because this was drafted behind closed doors, we will never know the real reason they decided the complexity and cost of granting tax benefits to pass-throughs were justified.

TCJA Encourages the Shift of Jobs and Profits Offshore: Despite the rhetoric about encouraging “American” multinational corporations34 to compete against “foreign” multinationals, the real effect of allowing multinationals to avoid taxes on profits they declare they “earned” offshore is to encourage them to shift their profits and jobs offshore.35

Although the act does include some alleged constraints on abusing this privilege — euphemistically called “global intangible low-taxed income” (GILTI) — they are so complex36 that the already understaffed IRS will be unable to effectively police them.37

***

In Part 2, Martin Lobel discusses how to prevent a taxpayer revolt.

Related front page panorama photo credit: Adapted by WhoWhatWhy from protests (Public Citizen / Flickr – CC BY-NC-SA 2.0) and (Public Citizen / Flickr – CC BY-NC-SA 2.0).

Endnotes

- “The Establishment” is defined as the Washington power structure, e.g. elected and unelected officials, lobbyists, etc. who make policy. Plutocrats are those wealthy individuals who influence or, in some views, control the Establishment.

- This article focuses only on the tax aspects, but we also need to update our antitrust laws which have not prevented the economic concentration that appears to be contributing to our economic problems. Tying Behemoths to Stagnant Pay and Low Growth, Neil Irwin, New York Times, Aug. 26, 2018, p, A1. For a discussion of other causes for middle class problems see, e.g. Steven Pearlstein, Can American Capitalism survive? Why Greed is Not Good, Opportunity is Not Equal and Fairness Won’t Make Us Poor (2018); Joseph E. Stiglitz, The Price of Inequality (2013); Hedrick Smith, Who Stole the American Dream, (2012); Donald L. Barlett & James B. Steele, The Betrayal of the American Dream (2012); Jacob S Hacker & Paul Pierson, Winner Take All Politics (2010)

- “Both parties are now led by highly educated voters whose interests are markedly different than those in the working class.” Thomas B. Edsall, Why Is It So Hard for Democracy to Deal With Inequality, New York Times, Feb. 15, 2018.

- This is not to suggest that economists are always right. As someone once quipped, economists predicted 9 of the last 2 recessions. But they are getting better. For a humorous look at the difficulty of getting economists to modify their mathematical theory of the rational person with perfect information decision making to incorporate insights from soft sciences, like psychology (a/k/a “animal spirits”) read Richard H. Thayer’s The Making of Behavioral Economics: Misbehaving (2015) . But they are working on trying to determine the causes of economic failures. See, Andrew Van Dam, How tariffs and corruption can ruin a growing economy, https://www.washingtonpost.com/business/2018/08/28/how-tariffs-corruption-can-ruin-growing-economy/

- https://tradingeconomics.com/argentina/gdp-per-capita

- https://tradingeconomics.com/united-states/gdp-per-capita

- In fairness, there were several hearings in the Senate but they were mostly for show. The bill had been drafted by the House in private consultations with chosen lobbyists. Most of the provisions discussed here were never exposed to public scrutiny before the bill was put on the floor of the House for a vote because Congressional leadership knew that, if the public understood what was in it, it would not pass.

- See, “Opportunities and Risk in Individual Tax Reform, Testimony of Lily L. Bachelder, Professor of Law and Public Policy, NYU School of Law, before the Senate Committee on Finance, Sept. 14, 2017 for a clear discussion of why TCJA fails these goals. See, also, the testimony of Kimberly A. Clausing, Professor of Economics at Reed College before the Senate Finance Committee on Oct. 3, 2017 on why the international aspects of business tax reform in TCJA fail these tests too.

- “Claims that behavioral responses could cause revenues to rise if rates were cut do not hold up on either a theoretical or an empirical basis.” Corporate Tax Reform: Issues for Congress, Congressional Research Service, Jane Gravelle, Sept. 22, 2017, Summary.

- Kansas: Exhibit A against trickle-down tax cuts, Jared Bernstein and Ben Spielberg, https://www.washingtonpost.com/news/wonk/wp/2017/06/15/kansas-conservative-experiment-may-have-gone-worse-than-people-thought/

- Kansas Tax Problems Loom Large in Federal Tax Reform, State Tax Notes Today, Oct. 17, 2017.

- Kansas Tried a Tax Plan Similar to Trump’s. It failed, Jim Tankersley, NY Times, Oct. 10, 2017. https://www.nytimes.com/2017/10/10/us/politics/kansas-tried-a-tax-plan-similar-to-trumps-it-failed.html.

- https://www.taxpolicycenter.org/taxvox/tax-policy-center-has-updated-its-baseline-tables

- https://itep.org/federal-tax-cuts-in-the-bush-obama-and-trump-years/

- You Know Who the Tax Cuts Helped? Rich People, Editorial, NY Times, Aug, 8, 2018, https://www.nytimes.com/interactive/2018/08/12/opinion/editorials/trump-tax-cuts.html; Robert Goulder, How I Learned to Stop Worrying About Buybacks, Tax Notes International, April 23, 2018, p. 599.

- E.g. William Lazonick, Profits Without Prosperity, Harvard Business Review, Sept. 2014. https://hbr.org/2014/09/profits-without-prosperity

- “To understand the magnitude of this shift [from dividends to stock buybacks], we analyzed financial data from 232 companies in the S.&P. 500 Index that were publicly listed in 1981, before the rule, and were still public through 2016. We found that from 1981 to 1983, these companies spent 4.3 percent of profits on buybacks. In comparison, from 2014 to 2016, these same companies spent 59 percent of their profits buying back their own stock. Dividends absorbed just under half of profits in both periods.” William Lazonick and Ken Jacobson, End Stock Buybacks, Save the Economy, Aug. 23, 2018. https://www.nytimes.com/2018/08/23/opinion/ban-stock-buybacks.html

- Stock Buybacks Are Booming, but Share Prices Aren’t Budging, Wall Street Journal, July 8, 2018. https://www.wsj.com/articles/stock-buybacks-are-booming-but-share-prices-arent-budging-1531054801

- https://www.washingtonpost.com/business/economy/beware-the-mother-of-all-credit-bubbles/2018/06/08/940f467c-69af-11e8-9e38-24e693b38637_story.html

- Economic Policy Institute, CEO compensation surged in 2017. https://www.epi.org/publication/ceo-compensation-surged-in-2017/

- Inflation Is Eating Away Worker Wage Gains, Paul Kiernan, Wall Street Journal, July 12, 2018. https://www.wsj.com/articles/u-s-consumer-prices-increase-at-fastest-annual-rate-since-2012-1531398709

- Rising U.S. Consumer Prices Are Eroding Wage Gains. Josh Mitchell, Wall Street Journal, Aug. 10, 2018.https://www.wsj.com/articles/u-s-consumer-prices-rose-0-2-in-july-1533904402

- https://itep.org/who-pays-taxes-in-america-in-2018/

- https://www.taxpolicycenter.org/taxvox/has-tcja-supercharged-economy-data-dont-show-it

- A Better Way: Tax Reform Task Force Report 25-26, (June 24, 2016, https://abetterway.speaker.gov/_assets/pdf/ABetterWay-Tax-PolicyPaper.pdf

- Paul Krugman, The Tax-Con Goes On, NY Times, August 23, 2018,

- U.S. Budget Gap Widens 21 percent in First 10 Months of Fiscal Year, Sharon Nunn, August 10, 2018,Wall Street Journal. https://www.wsj.com/articles/u-s-federal-budget-

- https://www.rollcall.com/news/policy/fiscal-2018-deficit-clocks-in-at-779-billion-white-house-reports

- https://www.cbo.gov/publication/53919

- https://www.taxpolicycenter.org/taxvox/what-would-it-take-congress-bring-federal-debt- down-manageable-levels

- Zoe Sagalow, Tax Cuts Not Prompting Most Firms to Hire or Invest, Survey Finds, Tax Notes, April 30, 2018, p. 746.

- Joseph DiSCillo, Proposed Regs Provide Guidance on Passthrough Deduction, Tax Notes, August 13, 2018, p. 1001.

- Stephen K. Cooper, JCT Figures on Tax Law’s Impact on Deductions Could Fuel Debate, Tax Notes Today, Aug. 24, 2018.

- Before TCJA Multinationals were actually paying significantly lower tax rates than before the 2008 financial crisis. The portion of profits they expected to pay in taxes had fallen by 9 percent. Rochelle Toplensky, Financial Times, March 11, 2018.

- About 40 percent of multinational profits are shifted to low-tax countries each year. or about 10 percent of the world’s GDP is held in tax havens, increasing the top 0.01 percent share of wealth. Alstadsaeter, Johannesen, Zucman, Who Owns the Wealth in Tax Havens? Macro Evidence and Implications for Global Inequality, NBEC Working Paper 23805.

- Ryan Finley, Proposed GILTI Regs Sent for OMB Review, Aug. 24, 2018, Worldwide Tax Daily; Alexander Lewis, News Analysis: BEAT Conflict Clouds Future of Pending Tax Treaties, Tax Notes International, Aug. 27, 2108, p. 885.

- Manafort, Cohen cases reveal weaknesses in enforcement of tax and election laws, Washington Post, Aug. 26, 2018, p. A1, Martin Lobel, The IRS is in Crisis and the Tax Community Needs to Help, Tax Notes, Dec. 14, 2015, p. 1407; reprinted in Huffington Post, Dec. 15, 2015.;