Saturday Hashtag #ShadowDebtCrisis

Welcome to Saturday Hashtag, a weekly place for broader context.

|

Listen To This Story

|

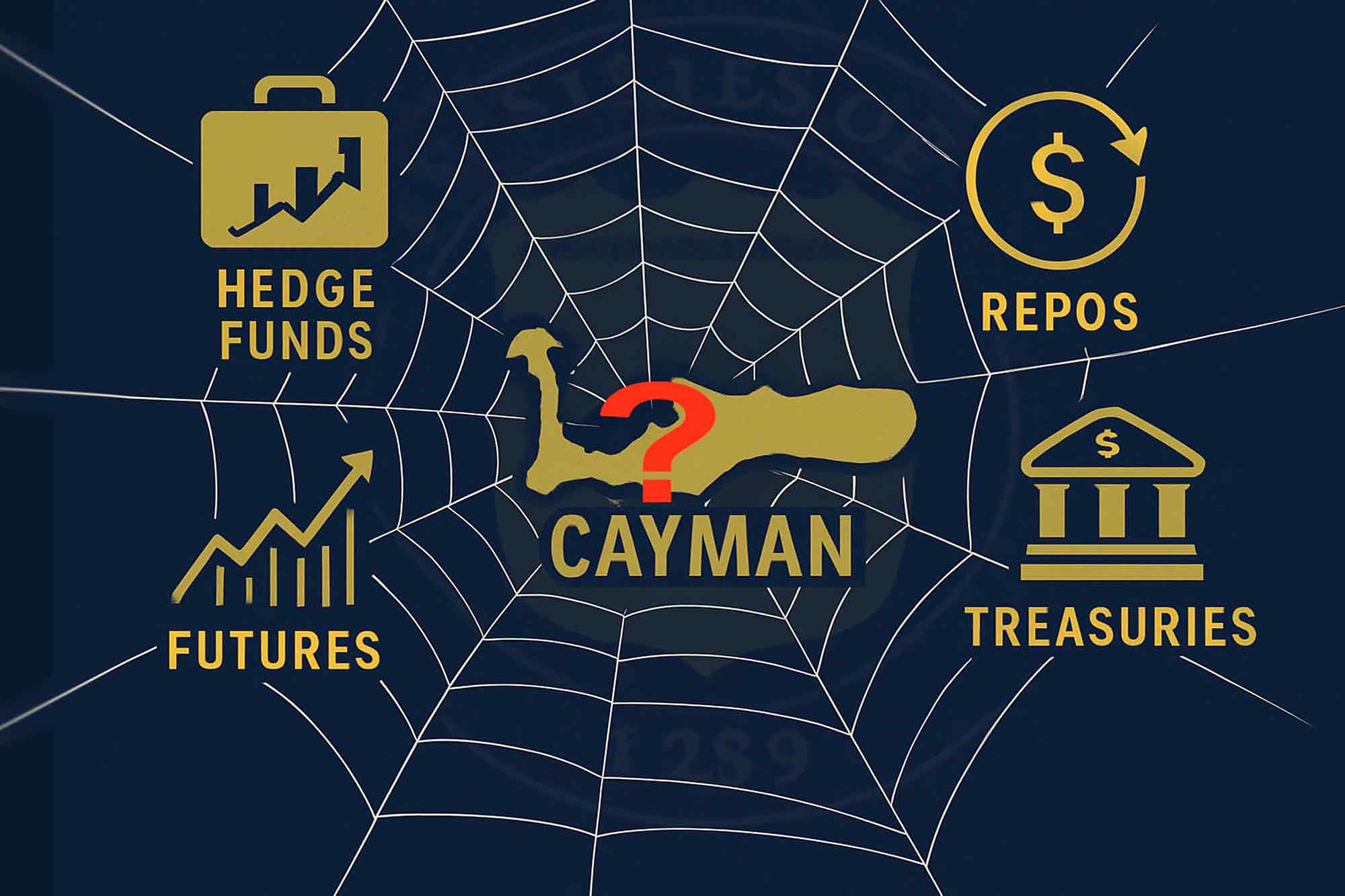

On October 15, the Federal Reserve released “The Cross-Border Trail of the Treasury Basis Trade.” It revealed a $1.4 trillion gap between two official measures of who owns US Treasury debt.

The Fed is actively investigating the discrepancy between Treasury International Capital (TIC) data, which tracks capital flows in and out of the US, and Form PF, data reported by SEC-registered investment advisers, regarding Cayman Islands holdings of US Treasuries.

TIC data show Cayman Islands entities hold only a small share of US Treasuries. But Form PF filings reveal Cayman-domiciled hedge funds held about $1.85 trillion at the end of 2024, $1.4 trillion more than TIC reports.

Between 2022 and 2024, these offshore funds purchased roughly 37 percent of all new Treasury issuance, making them key financiers of US debt.

Safe Bet To Systemic Risk

Hedge funds are using basis trades which profit from small price differences between two closely related financial instruments. In this case US Treasuries (government bonds) and Treasury futures (contracts based on those bonds).

They finance the bond purchases by borrowing cash in the hedge fund repo market, part of the broader $12 trillion-a-day repurchase agreement (repo) system. These are very short-term loans, that aren’t “loans” in the usual sense, but rather sales with an agreement to repurchase the same security later at a slightly higher price.

The borrowed cash is used to buy US Treasuries while the hedge funds sell Treasury futures as a hedge against those purchases. These loans are secured by the same Treasury bonds that the funds just purchased — meaning the hedge fund borrows cash to buy a bond and then uses that same bond as collateral for the loan it just took out.

Selling futures (a type of derivative) is simply selling a promise to deliver an asset or its cash value at an agreed price in the future. Usually this is a bet that the underlying bond price will fall and interest rates will rise.

But in this case, hedge funds aren’t betting on rates; they’re betting that the small price gap between cash Treasuries and futures will close smoothly and that funding will stay stable.

The danger is that this massive speculation operation is built on complex, private, and largely unregulated transactions that are heavily leveraged and sustained by rehypothecation, where the same collateral is reused across multiple loans throughout the financial system.

Rehypothecation is both the profit engine and fatal flaw of this system. The same collateral backs multiple repo loans, creating hidden fragility at scale. When trades unwind, lenders fight over loans that were never truly secured. Without it, leverage would shrink, profits would vanish, and the trade would lose its value.

Beyond the structural risk, this system also obscures who really owns the bonds. Official TIC data underestimate hedge fund holdings of Treasuries, while offshore structures, especially in the Cayman Islands, make it even harder to tell whether US debt is held by domestic or foreign investors.

The bottom line is basis trades only work in calm markets. They sink fast when volatility rises and if one thing is certain, the future is all about volatility rising.

Why Do You Care

- Hidden Risk: Treasuries are supposed to be the world’s safest asset, yet most of them now sit in the hands of highly leveraged hedge funds. This is a fragile foundation for the entire financial system.

- Rising Costs: If these trades unwind, demand for Treasuries could collapse, forcing the US to pay higher interest and driving up borrowing costs for everyone.

- Volatile Markets: Dependence on short-term repo funding means a sudden liquidity crunch could trigger mass selloffs, surging yields, and market chaos.

- No Transparency: Offshore hedge funds operate in the dark, leaving regulators and the public blind to the real risks behind America’s debt.

The Bigger Picture

For decades, foreign central banks like Japan’s ($1.1 trillion) and China’s ($7.5 billion) dominated Treasury purchases. Today, highly leveraged “offshore” hedge funds, effectively US or UK-based, have taken their place, chasing profits through complex debt-based trades. The world’s safest debt market now depends on fragile, short-term Wall Street speculation mechanics.

US debt is increasingly backed by opaque, covert funds rather than transparent stable foreign capital. The Fed report confirms this shift from official reserves to these private entities, masking a growing fragility, which signals a shadow US debt crisis in the making.

Hedge Fund Bets Against US Treasuries Threaten the Global Financial System

The author writes, “The build-up of US debt and hedge fund bets against US Treasuries have prompted warnings that a sharp sell-off in US government bonds could cause hedge funds to dump their holdings, setting off a doom loop that sends financial markets into a tailspin.”

The Cross-Border Trail of the Treasury Basis Trade

From the Federal Reserve: “Recent regulatory data collections on hedge funds indicate a massive increase in Cayman Islands hedge fund exposures to U.S. Treasury securities over the last two years, corresponding to a simultaneous surge in hedge funds’ Treasury cash-futures basis trade positions (the ‘basis trade’). While other data sources, including Coordinated Portfolio Investment Survey (CPIS) data, confirm this rise, statistics from official U.S. Treasury International Capital (TIC) data do not show a significant increase in Treasury securities held by Cayman Islands hedge funds.”

The Grossly Underestimated Hedge Fund Bid For Treasuries

From The Financial Times: “You might think that we have excellent data on the Treasury market and its inhabitants, given its systemic importance to the entire world. Ummm, no. Not even close. The reality is that we often have to try to smoosh together myriad awkward public and private datasets to understand what’s going on, and even then rough estimates and speculative assumptions are often still required.”

Sharp US Bond Selloff Revives Flashbacks of COVID-era ‘Dash-for-Cash’ (From April)

The authors write, “A violent U.S. Treasury selloff, evoking the COVID-era ‘dash for cash,’ has reignited fears of fragility in the world’s biggest bond market. The $29-trillion Treasury market had surged in recent weeks as investors dumped stocks for the safety of government bonds in a tariff-fueled risk-off shift. But on Monday, even as equities stayed under pressure, Treasuries were hit by a wave of selling that sent benchmark yields soaring by 17 basis points on the day, while trading within a yield range of about 35 basis points, one of the wildest trading swings for 10-year yields in two decades.”