Private banks are driven to increase profits for their shareholders. But what if banks were publicly owned and made their business decisions with the good of the local community in mind? Los Angelenos may put this notion to the test come November.

If Los Angeles were to establish a public bank — an issue its residents will vote on in the fall — one of two things could happen.

In the opinion of plan proponents, a public bank would free the city from predatory Wall Street institutions and save taxpayers a lot of money. That money could then be used to fund needed projects, such as affordable housing, infrastructure, renewable energy, and small-business expansion.

Opponents of the proposal, on the other hand, predict that such a bank would be a disaster. Untethered from market forces, the “public” bank might make loans to the politically connected without regard to profitable returns. Critics argue it would be so inefficient and poorly managed that city taxpayers would eventually be forced to bail it out.

Granted, even public approval does not mean LA will get a public bank. Other local, state, and federal hurdles need to be cleared before such a bank could be up and running.

Nevertheless, the vote on the measure could have implications far beyond the city or even California. If the proposal passes this November, it could jumpstart other efforts by cities and states around the nation that are currently considering setting up their own public banks.

New Jersey’s new governor was elected on a platform that promised to establish a public state bank. San Francisco and Oakland have done feasibility studies, though no results have been announced. In all, there are an estimated 15 separate pieces of legislation at the city and statewide level around the country that aim to establish local public banks.

Getting Off the Ground

.

Even before the Los Angeles City Council decided in late June to put the measure before the voters, there was controversy about how feasible public banking in LA was.

A report by the Chief Legislative Analyst’s Office in February raised a lot of doubts, including the initially high startup costs for the bank and a list of local and state laws that would have to be changed before it could even get off the ground.

“As Los Angeles City Council President Herb Wesson pointed out, if this were easy, someone would have done it already,” Sharon Tso and John Wickham, from the Office of the Chief Legislative Analyst for Los Angeles, told WhoWhatWhy.

Bank advocates disputed the findings of the report.

To start up a bank, all you need is $20 million, according to Ellen Brown, founder and chair of the Public Banking Institute. This figure is drastically lower than the one referred to in the initial report.

Because public bank supporter Gavin Newsom is likely to be California’s next governor, some think the legal and regulatory hurdles also can be surmounted. “Where there is a will, there is a way,” Brown said.

One source of startup funding: moving the city’s billions of dollars that now sit in checking and short-term investment accounts at commercial banks to the new public institution. Then the bank’s equity or reserve could come from either a city appropriation, voter initiative, bonds, or excess pools of interest earned by existing city budget items.

In any case, the bank would not be a retail bank. It would not accept retail checking and savings accounts from the general public. It would be a “banker’s bank,” with the City of Los Angeles acting as the primary customer and chief lender.

From the Ashes of the 2008 Crash

.

Without hesitation, some of the strongest advocates of public banking insist that this measure would never have made it onto the Los Angeles ballot had it not been for the crash and bailout of 2008.

“The crash of 2008 exposed the destructive flaws in the banking system,” Trinity Tran, co-founder of Public Bank LA told WhoWhatWhy.

People did not really feel the pain until after the 2008 crisis, concurred Mehrsa Baradaran, University of Georgia law professor and banking policy specialist.

The first steps of Los Angeles banking activists centered on convincing the Los Angeles City Council to divest city funds from what they considered to be predatory local banks. One of those groups, Divest LA, successfully persuaded the council to divest its accounts from Wells Fargo. The challenge then became where the city could deposit these divested funds.

Establishing a public institution became the next logical step. “Local banks are not big enough and aren’t able to collateralize loans,” Ellen Brown told WhoWhatWhy.

This type of political movement is not unique. After the Great Depression in 1929, there were grassroots movements for greater government intervention in the economy, explained Diego Zuluaga, a policy analyst with the Cato Institute.

Vote for the public bank this November! The Public Bank coalition (feat. GG team member @christopherroth) on stage at Ocasio-Cortez’s rally DTLA pic.twitter.com/QDfu3q0yTp

— Ground Game LA 👞👢 (@GroundGameLA) August 2, 2018

“In the 1920s and 1930s there was a promotion of farm lending and real estate lending to rural areas. In the 1990s it was all about home ownership,” Zuluaga told WhoWhatWhy.

A Shot in the Arm for LA, or a White Elephant for Taxpayers?

.

Public Bank LA has estimated that moving the city’s deposits from commercial accounts into a public bank would save local taxpayers $109 million in money that went to pay for annual and transactional fees to these commercial banks last year.

“Pulling Wall Street deposits and putting them into a public bank allows you to refinance existing bonds, and you can cut interest rates in half. With long-term loans, interest rates are 50 percent of the cost of financing,” Brown said.

Supporters refer to the example of Germany’s version of public banks. Sparkasse, a network of 400 regional public banks, has been instrumental, advocates claim, in implementing Germany’s green-energy transformation. They cite a statistic from Sparkasse’s chief economist that 73 percent of investment in renewable energy came from the German public bank sector.

And those are not the only benefits of a public bank, backers claim. A public bank would enable the city to loan money for badly needed affordable housing development. They believe a city-owned bank could extend the credit lines of community banks and credit unions to offer loans to low-income residents and help bankroll affordable housing.

Another benefit touted by bank promoters: badly needed investment in infrastructure. They hold out the example of Costa Rica’s public bank, Banco Popular. Advocates claim that this bank has been the financial linchpin behind the financing of water supply systems, residential solar panels, and hydroelectric generators.

“A public bank could make some investments that in the long-term would be profitable for LA… [investments that] no bank focused on short-term profit would dare to invest in,” Baradaran asserted.

A public bank is also seen by many as a means to local self-determination and bypassing high Wall Street interest rates. For example, LA public bank advocates estimate Los Angeles pays $3.14 billion in debt service, the cost to borrow money, from Wall Street. They argue a municipal bank would allow the city to recapture that money and give Los Angelenos a say in redirecting this funding toward local projects.

Others are less optimistic on how effective a public bank would be.

Critics point to a host of problems. They assert most public banks operate at a loss, are inefficient, and are high-risk ventures. Citing as examples the recent bailouts of Fannie Mae and Freddie Mac, quasi-public lending institutions at the federal level, they argue that public banks will eventually have to be taken over, bad debts and all, by the taxpayers.

Another criticism leveled at public banks is that they would make decisions based on political connections, not sound finance. Many believe loans from a public bank would wind up going to well-connected political players, not underbanked city dwellers.

Indeed, these critics also assert that public banks would eventually hurt those they are supposed to help. Many low-income and working-class families that initially benefited from low-income mortgage loans eventually found themselves in foreclosure.

“The verdict [on public banks] is scathing,” Zuluaga said.

Public bank supporters counter these arguments by pointing to the damage done by the 2008 bank crisis. They highlight how that financial meltdown cost millions their jobs, put millions out of their homes through foreclosure, and devastated the budgets of states and cities.

As one Occupy supporter and financial industry critic put it: “The most egregious failures of public banks can’t compare in impact to the damage done by private banks.”

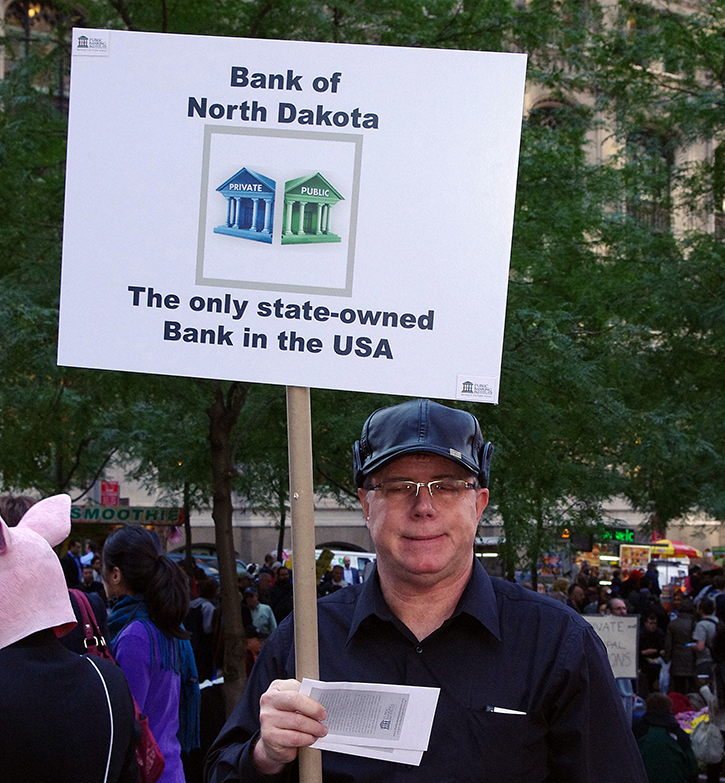

The North Dakota Model

.

Public bank allies use the Bank of North Dakota to advance their case. It is a public bank established almost 100 years ago, after an aggressive lobbying campaign by a populist party called the Non-Partisan League (NPL).

“The North Dakota Bank has a better credit rating than J.P. Morgan Chase, it’s more profitable than Goldman Sachs, it has a return on investment of 17%,” Tran said.

Others have a more skeptical view. Mark Calabria of the Cato Institute points out that many of the bank’s below-market rate loans go to the fossil fuel industry. This pattern, Calabria believes, bolsters the argument that many of recipients who benefit from the bank are both politically well-connected and financially secure.

This disagreement over the performance of the Bank of North Dakota also extends to how both sides have viewed the historical performance of public banks.

Calabria regards public banks as almost consistent failures, starting in colonial times when they were first tried. The first American public bank, the Vermont State Bank, was established in 1806. Calabria claims it failed six years later, costing the citizens of Vermont the equivalent of almost $3 billion in today’s money.

Calabria adds that seven other states established public banks in the 1800s with the last of these, the Bank of the State of Indiana, closing in 1859. All of these banks were characterized by rampant corruption, according to critics.

Advocates see the history of public banking in a radically different light. They point to the successful American colonial experience with land banks, an idea promoted by none other than Benjamin Franklin. And, advocates argue, the Vermont State Bank is an argument for better regulation of public utilities, not an argument against public banking.

Different World Views

.

These starkly different world views reflect how both sides assess the value of commercial, private banks.

Public bank supporters see private banks as predatory agents, charging Los Angeles rip-off interest rates and fees that enrich themselves at the city’s expense. They also view those banks as using the city’s money to finance projects that are socially destructive to Los Angeles.

They hold Wall Street responsible for bubbles in housing and capital markets — bubbles that later caused the financial crash in 2008.

Public bank detractors have a much different take. “Bank fees are going to institutions that help Los Angeles. [Fees are] going to pay for the provision of services and the intermediation funds between LA and other places. [Fees pay for] professionals to do due diligence and risk management [for the city],” Zuluaga stated.

Public bank advocates see greater governmental regulation of predatory lending and the creation of public institutional alternatives as needed steps to check the power of Wall Street.

Detractors believe too much government regulation of banks has led to more expensive bank services. Also, failure is not punished in the banking system, according to many of these critics. Exposing financial institutions to greater risk is part of the solution, Zuluaga asserted.

Will Public Banks Bring the Cannabis Industry’s Financing Above Ground?

.

The perceived need to bring the financing of the cannabis industry above ground was one motivation behind the current drive for the Los Angeles public bank.

“We’ve got people that are going to go home tonight and sleep on a mattress that’s worth $2 million,” Los Angeles City Council President Herb Wesson said. He was referring to cannabis business owners who stash their profits at home instead of a bank.

This is because federally insured and regulated banks have refused to handle transactions involving cannabis, which the federal government still considers an illegal drug.

California’s $8-20 billion cannabis industry is still operating mostly in cash almost two years after state legalization, with the majority of businesses paying no taxes, according to California State Senator Fiona Ma.

“It doesn’t make any sense to legalize the distribution [of cannabis], then you make the money gained from that distribution illegal to put in the bank,” Baradaran asserted.

On May 30th, 2018, the California State Senate passed legislation allowing state-chartered banks and financial institutions to apply for a special cannabis banking license.

Other public bank advocates reject the notion that cannabis industry finances are the driving force behind the measure. “This is first and foremost a people’s bank. It’s here to work in the economic and social interests of the people of Los Angeles,” Tran insisted.

Can the LA Vote Jump-Start Public Banks Nationwide?

.

If the second largest city in the nation votes in favor of the initiative this November, it would generate momentum in other states and cities that are looking at legislation to create their own public banks.

https://www.youtube.com/watch?v=D80KEVbAGjA

At the same time, advocates of public banks will have to overcome the formidable private bank lobby. If the past is any guide, initiative supporters will be heavily outspent.

But public bank supporters get solace from a successful California initiative on the 2016 ballot, Measure HHH. The goal of this measure was to pass a bond that would help fund 10,000 units of housing for homeless residents.

“Voters passed Measure HHH by 77%. That was a victory determined by the ability to organize across a very broad sector of community-based groups,” Tran said.

Ballot initiatives have often blazed new trails that later spurred legislation and shaped policy. In Los Angeles, 10 years after commercial banks plunged the world economy into a crisis, voters will have a chance to jump-start alternatives to conventional private banking.

Related front page panorama photo credit: Adapted by WhoWhatWhy from Los Angeles (David Seibold / Flickr – CC BY-NC 2.0).